Restraining Notices: What Are They & How Do They Work?

Under New York CPLR § 5222, once a creditor has gotten a judgment for a debt, it has the right to use something called a "restraining notice" to freeze assets—including your bank accounts—to "satisfy" the judgment.

Here's how they work. A restraining notice can be sent to the debtor or to anyone the creditor believes is holding assets that belong to the debtor. The notice puts the person who receives it on alert that the assets should not be sold, disposed of, or interfered with. Hiding or disposing of assets that are subject to a restraining notice is contempt of court and is punishable with fines and jail time.

Either the clerk of court or the creditor's lawyer can issue a restraining notice. Generally, the notice may be served personally or by certified mail, although regular mail and electronic service are allowed when the state serves retraining notices related to support and custody obligations.

It should be noted that restraining notices are not used in the case of wage garnishments to employers.

Restraining Notices Have Specific Requirements

Under New York law, there are very specific requirements for the content of a restraining notice. It needs to include:

- The names of all the parties in the case for which the judgment was obtained;

- The date and court where the judgment was entered;

- The amount of the judgment or order and the amount currently due;

- The names of all the parties in whose favor a judgment was entered;

- The names of all the parties against whom judgment was entered;

- Specific language explaining that property the debtor owns or has an interest in is being sought to satisfy a debt and that sale, assignment, transfer, or interference is forbidden and will be considered contempt of court;

- A copy of the judgment.

Also, as noted in a prior blog, a "Notice to Judgment Debtor or Obligor" must be sent to the judgment debtor within one year of service of the restraining notice.

What Money is Exempt under New York Law?

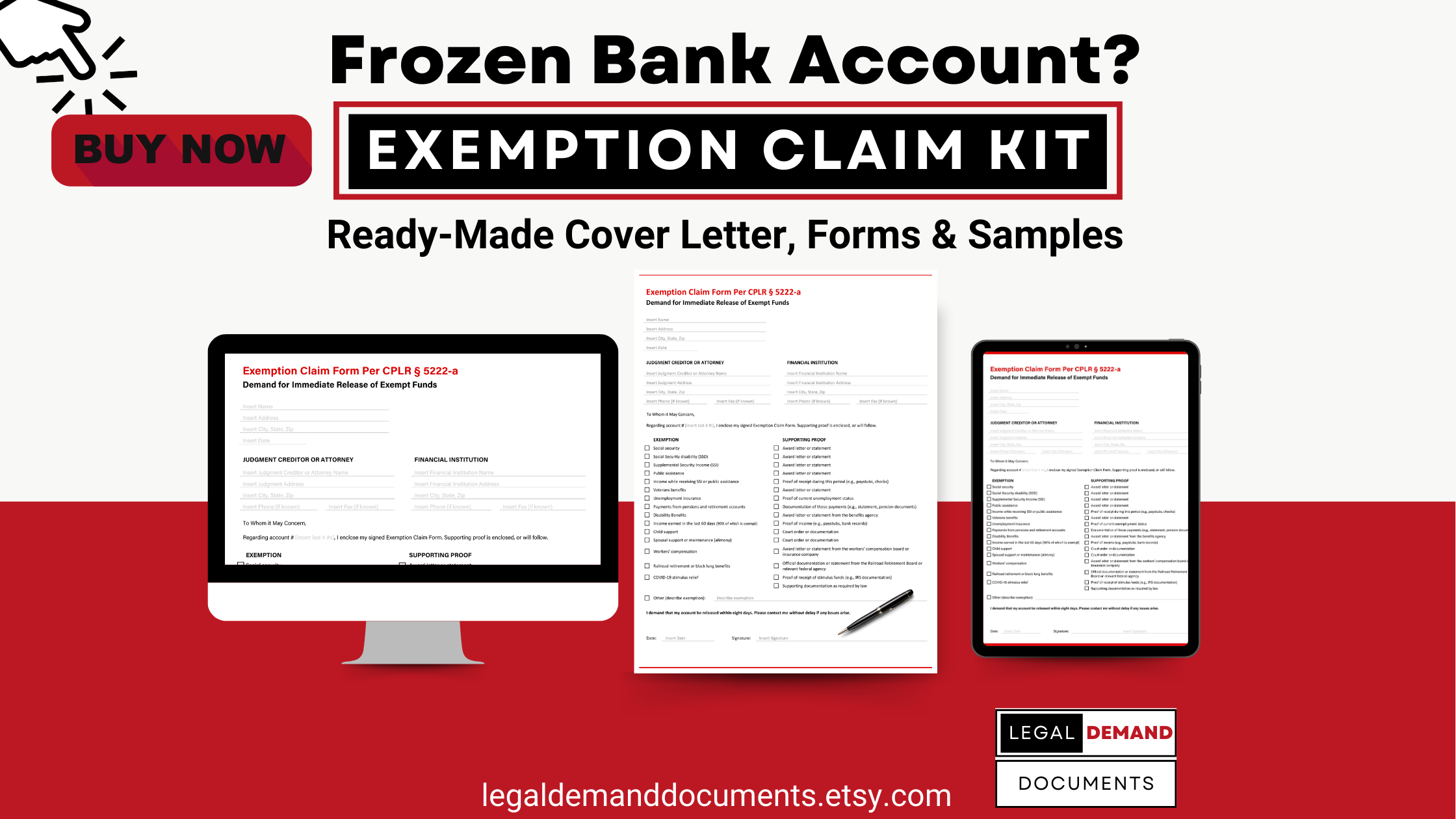

There are also specific exemptions from the creditor's right to freeze assets using a retraining notice. Unless the debt relates to child support, spousal support, maintenance, or alimony, the following types of income are exempt from being frozen:

- Supplemental security income (SSI);

- Social Security;

- Public assistance (welfare);

- Spousal support;

- Alimony/Maintenance;

- Child support;

- Unemployment benefits;

- Disability benefits;

- Workers' Compensation benefits;

- Public or private pensions;

- Veterans benefits;

- 90% of wages or salary earned in the past 60 days (with some limitations);

- Railroad retirement;

- Black lung benefits;

- Statutory exemptions based on necessity and minimum wage: $3,600.00 (NYC); $3,120.00 in Nassau, Suffolk, and Westchester; $2,832.00 in all other counties in the state. These amounts are automatically protected in your bank account. These were raised based on an increase in the minimum wage in 2019.

- $3,000.00 protected if any direct deposits from identifiable exempt sources (i.e. social security, unemployment, pension; see below) were made within the last 45 days.

In spousal support, alimony/maintenance, and child support cases, the exemptions do not apply. The state can claim otherwise exempt funds to satisfy an outstanding support obligation.

When a restraining notice is served, a separate notice needs to be sent to the debtor explaining the exemptions and the debtor's right to consult an attorney about a claim of exemption. An exemption notice may not be required in some situations related to repeat restraining notices within a 12-month period. The exemption notice can be personally delivered or mailed. If mailed to a work address, it must be marked "personal and confidential" and must not disclose on the outside of the envelope that it relates to a debt. There are very specific requirements contained in New York CPLR §5222 for the contents and language of the exemption notice.

After a restraining notice has been served, unless an exemption applies, the recipient of the notice should treat the assets covered by the notice as "frozen" until they either receive instructions from the court regarding the liquidation of the assets or receive notice that the judgment has been satisfied or vacated.

The Mechanism of A Bank-Account Freeze through Restraining Notice

A creditor restraining notice, in relation to consumer banking, is a judicial tool used by creditors to momentarily halt or "restrain" the activity of a debtor's bank account. This measure is commonly enforced following a judgment favoring the creditor, thereby enabling them to earmark funds from the debtor's account to settle the outstanding debt.

This restraining notice is delivered to the bank, bypassing the consumer, and it prohibits the bank from permitting the debtor to make withdrawals or payments from the seized account up to the judgment amount. Nonetheless, there are certain safeguards and exceptions instituted to ensure that a debtor retains access to some funds for essential living costs.

For instance, according to the New York Civil Practice Law and Rules (CPLR) Section 5222, some funds, such as a specified minimum balance or money received from particular sources like Social Security or disability payments, are not subject to restraint. This protection allows the consumer to continue to meet basic financial responsibilities amidst the process of debt retrieval. It's crucial for consumers to comprehend these rights and consider seeking legal advice if a restraining notice is served on their bank account.

Synopsis of CPLR § 5222. Restraint Notification

This abstract of CPLR § 5222 provides a simplified and comprehensible recap of the actual legal statute. The original statute is filled with legal jargon and statutory language, often challenging to grasp for individuals without legal training.

CPLR § 5222 regulates the process of issuance and delivery of restraint notices and the specifics regarding what it means for judgment debtors and those possessing the debtor's property.

(a) Issuance and Delivery of Restraining Notice: The court clerk, the creditor's lawyer, or the support collection unit issues a restraining notice meant to put a freeze on a bank account. This notice is served to everyone but the debtor's employer when the property in question is a salary or wage. It's delivered personally, by registered or certified mail, regular mail, or electronically. It contains details of the judgment or order and a warning about possible contempt of court penalties for non-adherence. A revised notice is served if the interest rate changes during a restraint period.

(b) Implication and Duration of Restraint: On receipt of the notice, the debtor is prevented from transferring or meddling with any property they own, unless directed by the court or sheriff, until the debt is paid or the order lifted. Any property or debt in the debtor's possession becomes subject to the notice. Individuals who aren't the debtor but are served the notice should not transfer or dispose of any involved property or money until the judgment is satisfied, vacated, or a year passes.

(c) Subsequent Notices: Court permission is necessary to serve more than one restraining notice on the same person for the same judgment. A creditor is not allowed to serve more than two notices per year on a natural person's bank account. If the interest rate changes during a restraint, a revised notice is issued without court permission.

(d) Notification to Judgment Debtor or Obligor: If the debtor hasn't received a notice within a year before the restraining notice, a copy of the restraining notice, along with the notice to the debtor, should be mailed to them within four days of serving the restraining notice.

(e) Content of Notice: The debtor's notice should inform them that their money or property may have been seized or held to settle a judgment and provide a list of money or property types exempt from seizure to satisfy judgments.

(f) "Order" Definition: An "order" in this setting refers to a directive from a competent court demanding payment of support, alimony, or maintenance upon which a "default" has been established.

(g) Electronic Restraining Notice: With written consent, a restraining notice can be served in an electronic medium, such as magnetic tape. However, notice to the debtor must still be given in written form.

(h) Impact on Accounts Receiving Exempt Payments: If an account has received direct deposits of statutorily exempt payments within the 45 days before the notice, the bank should not restrain $2,500.00 in the debtor's account. If the account holds less than this amount, the notice is null.

(i) Implication for Debtor's Banking Account: A restraining notice should not apply to sums equal to or less than 240 times the federal or state minimum hourly wage, whichever is larger unless a court determines the amount is not necessary for the debtor's reasonable needs.

(j) Bank Fees for Processing Restraining Notice: If a bank served with a restraining notice cannot lawfully freeze a debtor's account, or a freeze is imposed in violation of any section of this chapter, the bank should not charge the debtor any fee.

(k) State of New York as Creditor Exceptions: The provisions in sections (h), (i), and (j) don't apply when the creditor is the state of New York

![]()

Contact us 888-271-7109 immediately if your bank account has been locked up.